Meeting Note

China Pursues Structural Transformation

- The political outlook of China’s top leaders has become more conservative after the trade war and the pandemic elevated their sense of insecurity

- This will endure until 2027, when a new generation equipped with more experience both abroad and domestically rises to China’s leadership

- Beijing’s reluctance to support the economy stems from its limited policy tools, satisfaction with current economic data, and determination to reduce structural reliance on real estate

- China’s leaders may yet take action in the face of a crisis or deviation from targets

Hutong Research’s partners just concluded a two-week tour through Hong Kong, Singapore, Oslo, and London—our largest client bases outside of mainland China. During this trip, we met with dozens of current and prospective clients to present our base case, 2024 outlook, and sectoral projections. This note addresses some of the key questions and our responses.

How should one understand Beijing’s policymaking today?

Before delving into specific policies, we were asked about the political mindset and vision of China’s current leadership. This is where we add the most value: Instead of merely reporting on events, we help clients grasp the fundamental political dynamics that drive the fast-paced policy actions and lane-changes seen on the surface.

We argue that the current five-year period (2022-2027) is the most peculiar in China’s modern history and features a shift in political mentality. Specifically, today’s leaders are more conservative than their predecessors and feel deeply insecure amid external “changes unseen in a century.”

This conservatism is a product of their formative years. Born in the mid-1950s, they came of age in a Leninist society that acculturated them to greater party control over all aspects of life. The Cultural Revolution also delayed or disrupted education for most of them.

As the first generation of leaders to experience the entire reform era, they once firmly believed in the effectiveness of long-term economic planning, as well as Deng Xiaoping’s famous edict that “problems raised in development can only be solved by development.” It is worth recalling that many of the leaders today taking flak from the market were praised for supporting the private and internet-based economy while in local-government roles just a decade ago.

The situation began to change just as they rose to the top party echelons in the mid-2010s, with the advent of the Donald Trump presidency in the US and the COVID-19 pandemic.

First, these “black swan” events exposed the flaws of long-term planning. Second, they highlighted the importance of security especially in nonconventional areas such as supply chains and public health.

Third, these leaders’ rise coincided with the worldwide internet boom, which reapportioned control over public discourse and agenda-setting from the Party to social media. This exaggerated their sense of insecurity, as the Party has long viewed propaganda as its lifeline.

Felt both domestically and internationally, this insecurity poses an urgency for China’s leaders to adopt a different approach. Four main guidelines are shaping Beijing’s reaction.

First, party and government institutions should be less restrained by norms and rules, to stay agile and adaptable to “black swan” events. This has led to the creation of party central commissions, which are more flexible in personnel and their decision-making process, on top of State Council ministries that are governed by whole sets of laws and regulations.

Second, Beijing should dispense with binding and long-term economic targets to avoid the embarrassment of under-delivery. Economic plans and targets have thus become superficial, and policies more reactive and ad hoc than pre-emptive.

Third, Beijing should also endeavor to solve problems as soon as possible, as longer delays compound the uncertainty. For example, Beijing’s expansion of college admission in 2019 to offset US-China trade war’s impact on youth employment that year inadvertently worsened the problem four years later as the move led to more college graduates entering the job market during the pandemic.

Fourth, the Party should exert more control over emerging technologies to prevent societal disruption—hence a rebalance between security and development. In practice, this means identifying security considerations and assessing all risks before actual policymaking, which often results in policy actions that are both conservative and delayed. This is exacerbated by stakeholders’ varying and often conflicting interests. (See: What Will Shape China’s Policymaking in 2024).

That said, we expect a significant change in mindset with the next generation of leaders, who will accede in 2027. Now in the Politburo, they are within China’s first generation of university graduates and, in many cases, studied abroad. They have also spent significantly more time in different regions of China and functions as officials, as Xi Jinping has been grooming them since the mid-2010s. This makes them more experienced in statecraft than the incumbents, whose promotions to the top were expedited by Xi.

People to watch in this coming generation include party secretaries Chen Jining of Shanghai and Yuan Jiajun of Chongqing, as well as Beijing mayor Yin Yong. Chen spent 10 years in London, Yuan is a fluent Anglophone and aerospace engineer by training, and Yin is a Harvard Kennedy graduate with work experience in Singapore.

Why has Beijing not supported the economy more?

Coming to actual policies, Hutong’s partners were then asked about Beijing’s reluctance to provide more support to the economy. We attribute this mostly to the third abovementioned guideline, in that Beijing seeks to solve problems as they arise rather than delaying, as it sees current economic data as satisfactory and structural adjustments as inevitable.

Last year, Beijing targeted 5% growth and ultimately delivered 5.2%. Its goal was thus met despite market dissatisfaction with deflation and poor corporate profits. Behind the headlines, household consumption appears to be recovering, exports are improving, and industrial profit growth is also rebounding. Overall, real estate seems to be the only area in need of policy support.

Nonetheless, Beijing is determined to reduce China’s reliance on this sector following a key lesson learned. That is, help given to real estate via the “shantytown” redevelopment campaign of 2015 ultimately only delayed necessary structural adjustments and made them more painful (See: What Can China’s Three Projects Accomplish?).

Meanwhile, the current momentum of consumption and services provides a rare window, if not the last one, to shift China’s growth model to be driven by those sectors rather than by real estate and investment. In 2023, services led China’s recovery despite the collapse of real estate, and consumption contributed to over 80% of growth. Policies only needs to sustain this existing trend.

Consumption of services was particularly strong, with double-digit growth in household expenditure on transportation, communications, entertainment, and healthcare. A stronger service sector will help alleviate unemployment among the youth, who are less interested than ever in manufacturing and are entering service jobs at a rate of 70%.

In addition, there is little more support that Beijing can offer to stimulate the economy. Monetarily, it has been lowering rates since 2019 but with diminished effectiveness—and further cuts could depreciate the RMB unless the US Federal Reserve also cuts its own rates.

On the fiscal side, state investment has already been outpacing private for two years; doubling down on the former could crowd out the latter even more. At the same time, local governments’ top priority is to mitigate their debt risks, so they must invest frugally (See: Beijing Targets Provinces with High Debt Risks).

Nonetheless, energy-related investments will continue to receive strong backing. This is because Beijing regards the green-energy transition—domestically and globally—as a cornerstone of both security and development. The sector further affords an opportunity for China to increase its global influence, as Xi highlighted in last week’s study session (See: Xi Doubles Down on Green Energy Transition).

Meanwhile, Beijing is prepared to react to economic crises and deviations from targets. This was already proved this year with the appointment of Wu Qing as head of the China Securities Regulatory Commission and the 5-year LPR rate cut. (See, respectively: Beijing Appoints New Top Securities Regulator and Beijing Attempts to Stabilize Housing Sales).

In other words, Beijing will likely wait for more data before announcing further policy support. Looking ahead, daily housing sales remain the highest-frequency data to watch, followed by monthly credit and trade data to be released in mid-March. Then, after the release of Q1 GDP data in mid-April, the Politburo meeting towards end of that month will be the most critical sign by which to read Beijing’s assessment of the economy and forecast any policy changes.

How would Beijing react to another Trump presidency?

Another question that Hutong received was on Beijing’s attitude towards the upcoming US presidential election. Trump appears to be the current frontrunner, and significant tariffs on Chinese goods would be in the cards if he wins. Clients worry that another round of Trump would further stifle China’s fragile economy.

We first argue that a Trump victory is still far from certain, as polling data will only become reliable after May, when the candidates start to campaign in earnest.

Second, Beijing likely views a second term for Biden as no better for China’s economy than one for Trump: While the latter portends higher tariffs and a more hawkish disposition overall, the former would beget better policy articulation and a more coherent anti-China narrative. Biden’s policy battery could be more credible to the US public and even more damaging to China.

Third, a Trump sequel may be an occasion for China to repair its relationship with the EU. After all, Trump was hawkish not only towards China but also the US’s own allies and the US-led system of global governance overall.

A Trump win may herald tariffs on imports from the EU, withdrawal from global cooperation on climate change, and rescission of support to Ukraine. Such actions could, to the EU, paint the US as a greater risk to global stability than China.

In fact, China-EU relations did improve once with Trump in the White House. In March 2018, Trump announced tariffs on steel and aluminum imports from all trading partners, as well as additional tariffs on many Chinese goods. In June that year, China and the EU issued a joint statement for the first time in three years, with a focus on areas of common interest like clean energy and WTO reform.

Given this, the EU’s ongoing anti-subsidy investigation into electric vehicles (EVs) from China may offer a channel for communication between the two. After all, the results are not due until November, and final measures could range from price floors to tariffs and cover not only Chinese firms but others like Tesla. The precise impacts of these measures on China will vary widely, so will Beijing’s responses.

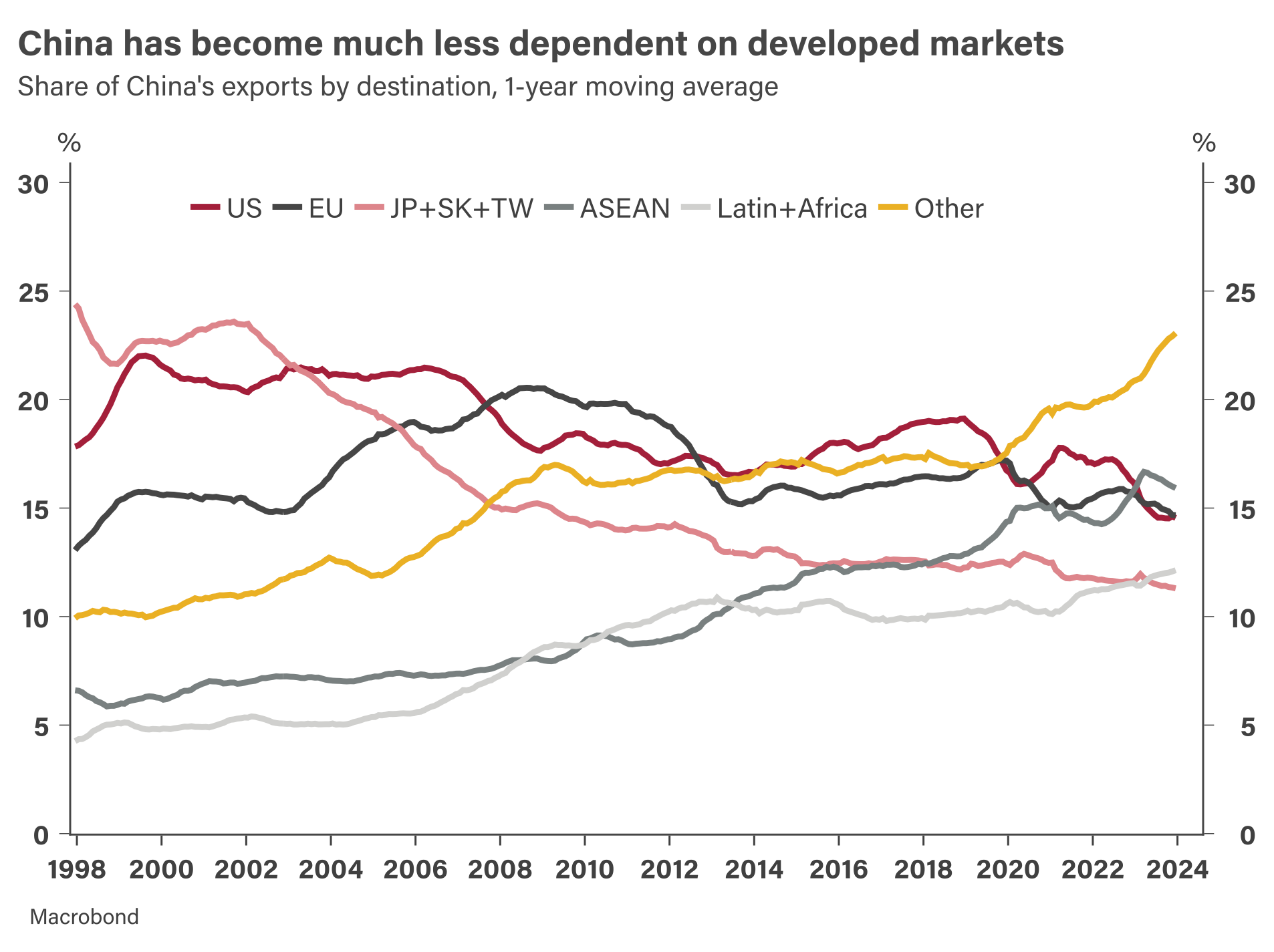

Meanwhile, China is diversifying its export market to hedge against potential tariffs from either or both the US and EU. Only 14.5% of China’s exports in 2023 were US-bound, down from 19.1% in 2018. The EU’s share also fell to 14.6% from 16.5% in the same period. On the other hand, China’s exports to developing countries have surpassed those to developed ones. Even in EVs, exports to the EU declined to 41% in 2023 from 47% in 2022, meaning faster export growth to other countries.

Beijing is also facilitating and encouraging domestic firms to invest abroad. Ones along the automotive supply chain are moving to Mexico and Hungary for the US and EU markets, respectively. This was greenlit by top leaders in China: Foreign minister Wang Yi received his Mexican counterpart Alicia Barcena in December and pledged to strengthen bilateral cooperation. In October, Xi met Hungarian premier Viktor Orbán, the only EU attendee of China’s Belt and Road Forum.

Meanwhile, Beijing is trying to attract more foreign direct investment (FDI), especially in high tech and research and development (R&D). On 23 February, premier Li Qiang discussed further measures to this effect during a State Council executive meeting. In light of export controls against its purchase of advanced tech, China can only rely on FDI to develop its own.

Finally, China will increasingly rely on state-owned enterprises (SOEs) to supply essential goods and to invest in strategic sectors. Following the trade war and the pandemic, it has come to view SOEs as an important pillar not only of the economy but also society and party control. In practice, that means that political mandates will carry more weight for SOEs in sectors like food and energy. At the same time, SOEs overall will be asked to pay out more dividends and divest from nonstrategic sectors, so that Beijing can redistribute capital towards areas that it deems more important.

© Hutong Research. Redistribution prohibited without prior consent. This report has been prepared for distribution to Hutong Research clients. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. For more information and research archive, visit: www.hutongresearch.com