China Economy

Listed Companies in China Slump Further in Q3

- A-share nonfinancial listcos in China performed even worse in Q3

- Industrial listcos face fierce competition from smaller peers that sacrifice profit for revenue, while service listcos are cutting headcounts to maintain profitability

- Beijing’s trade-in campaign offered crucial support to relevant industries

- Listcos are slashing investment amid poor profitability—but their smaller peers are investing regardless, likely enabled by government support

- Most industries have less cash and more accounts receivable, which will squeeze their working capital

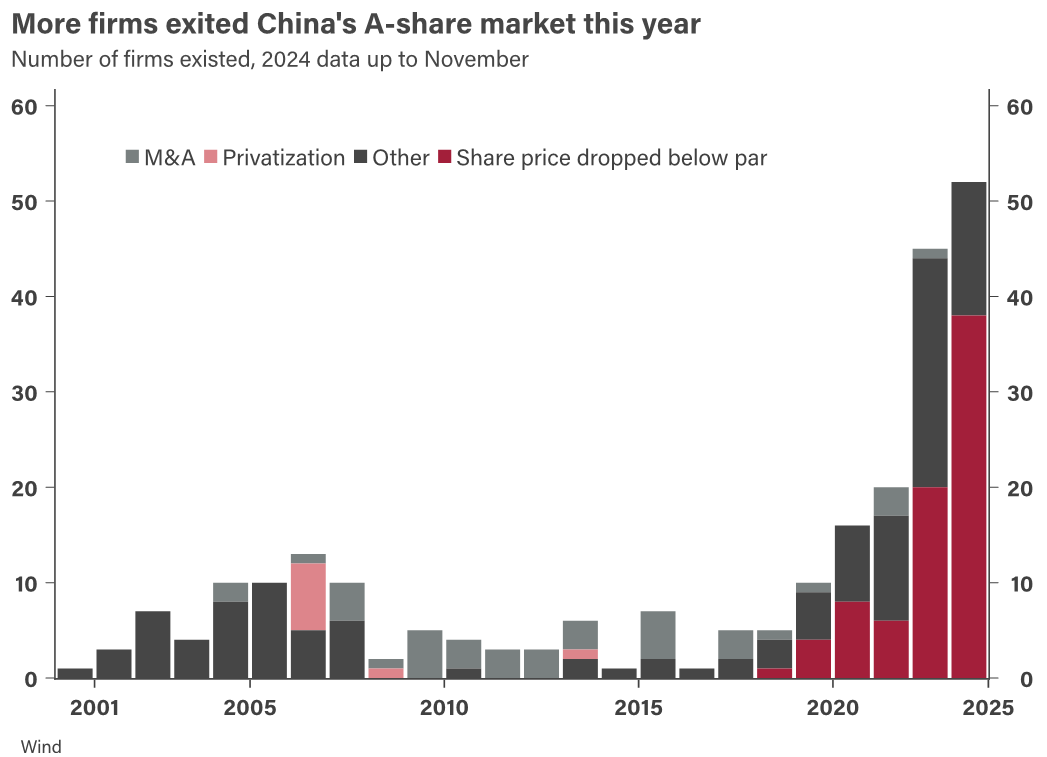

- More firms exited and fewer entered China’s A-share market; IPOs may recover only after share prices stabilize and Beijing’s anticorruption drive winds down

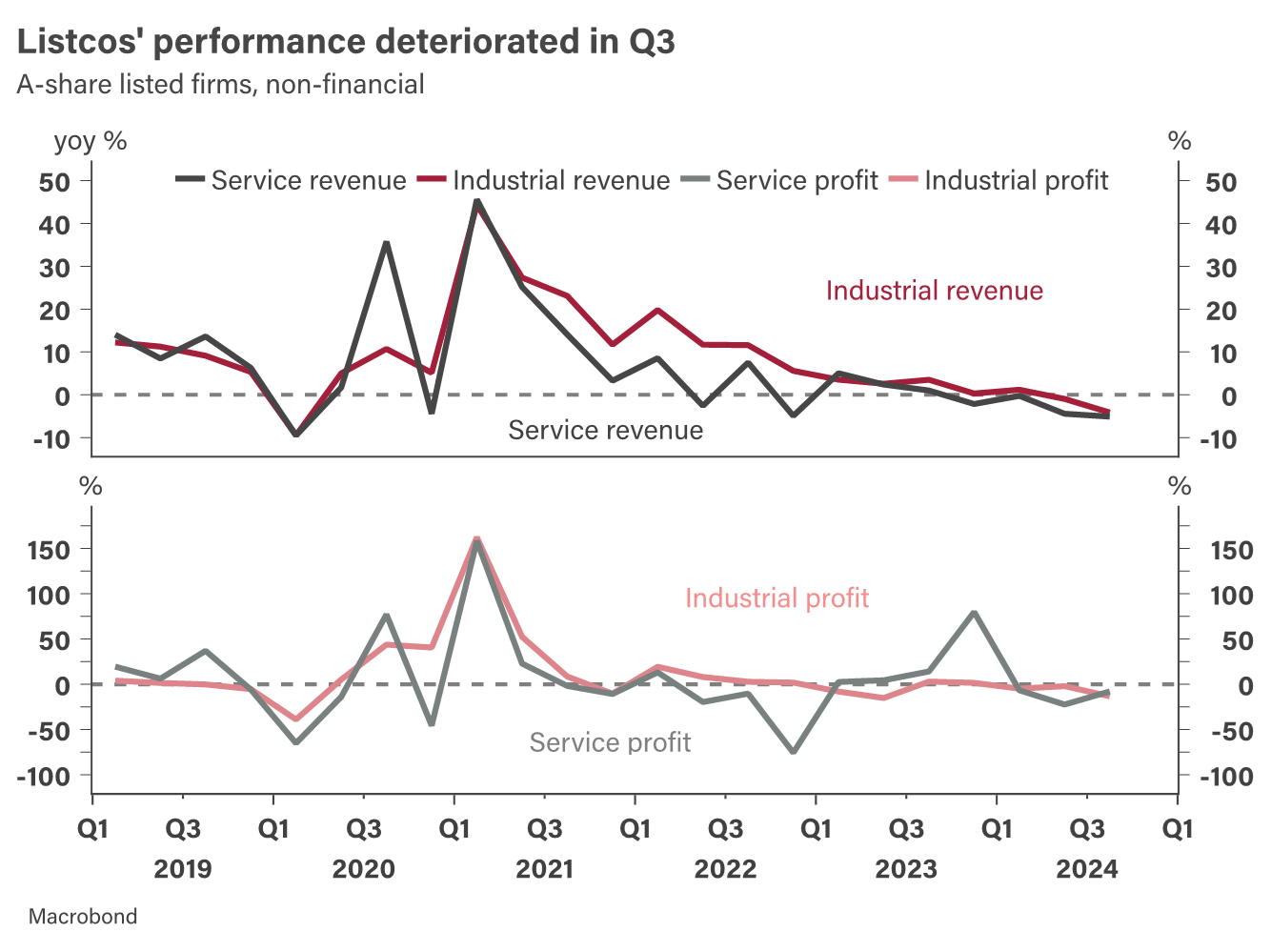

China’s A-share listed companies’ performance deteriorated further in Q3—the worst-performing of the year. Based on their financial statements, nonfinancial listcos collectively reported RMB 15.3trn in revenue and RMB 1trn in profits, down by 4.2% and 10.6%, respectively, yoy. Year-to-date revenue and profits fell by 1.7% and 7.1%, respectively, yoy.

Industrial listcos recorded yoy falls of 4.1% and 13.2% in revenue and profit, respectively, for Q3. The National Bureau of Statistics (NBS), however, found revenue growth and profit decline of 0.6% and 15.2%, respectively, yoy. These differences—which arise because NBS tracks all industrial firms with annual revenues over RMB 20mn, while nearly all listcos exceed RMB 100mn—suggest that larger firms are facing fierce competition from smaller ones, which are pursuing revenue even at the cost of profitability.

Versus industrial ones, service listcos saw their revenue fall more and profits fall less—by 5.1% and 7.9%, respectively, yoy. Service firms thus appear to have enacted more aggressive cost cuts, which improved their margins but resulted in more layoffs given their labor-intensity. Indeed, service listcos’ numbers of employees have declined by 8,200 since the start of the year, while those of their industrial counterparts have increased by 5,300.

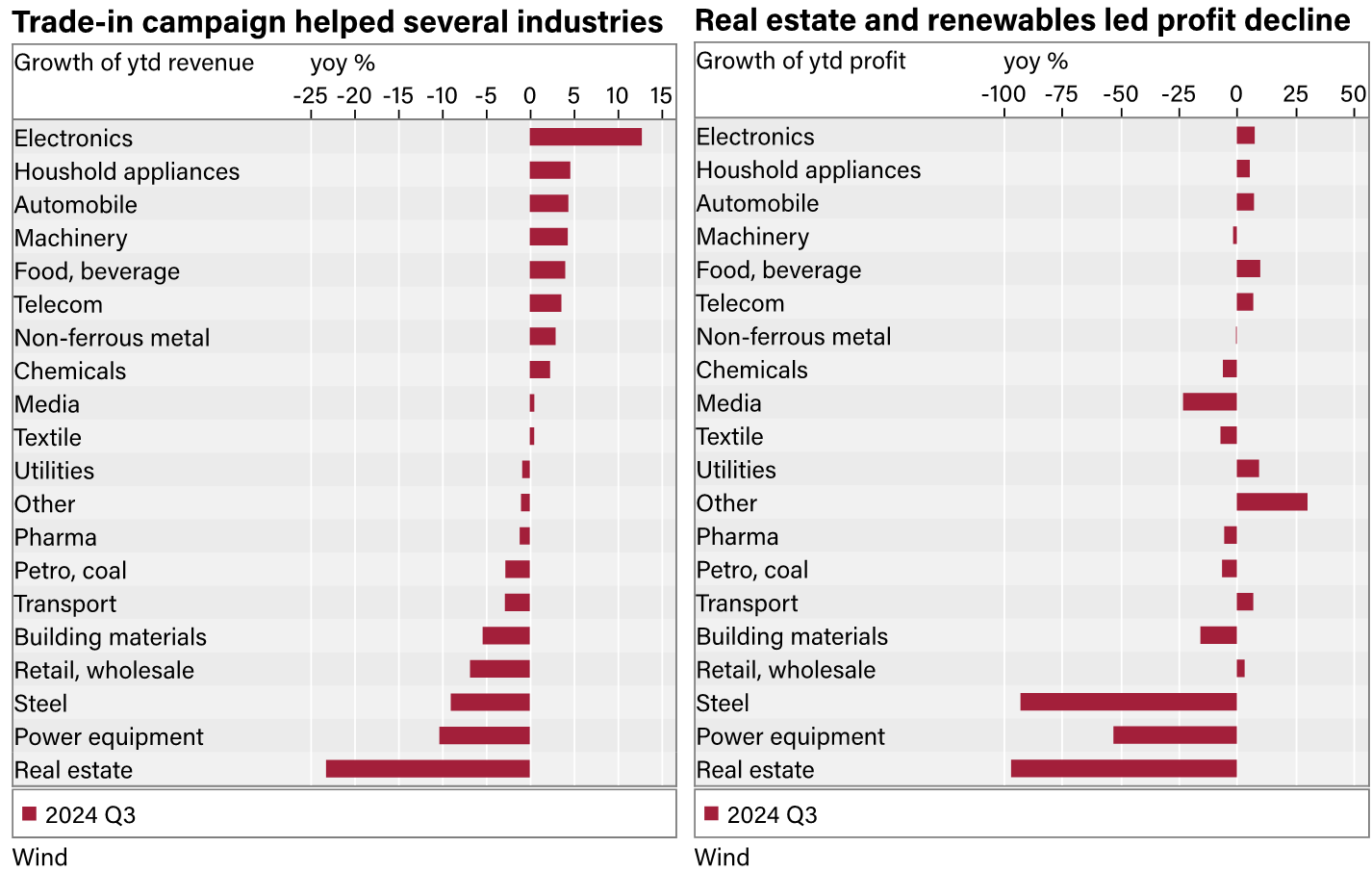

Analyzed by sector, electronics led the growth with year-to-date revenue up by 13% yoy, followed by yoy increases above 4% each by household appliances, automobiles, and machinery. The outperformance of electronics is largely cyclical, as global consumers upgrade their devices, while strong growth in the latter three likely results from Beijing’s trade-in campaign. Said campaign covers not only consumer goods such as household appliances and automobiles but also equipment upgrades.

Thanks to these campaigns, the appliance and automobile industries respectively earned 6% and 7% more in profit than a year ago. In automobiles, though, most was earned by firms that produce auto parts rather than by automakers themselves. Year-to-date, the former’s profit growth is 21% yoy; the latter suffered a 7% yoy decline. More worryingly, the former hired only 2,000 more people so far in 2024 versus the latter’s 9,500 more. Machinery, which hired 30,000 more people, recorded a 2% yoy profit decline despite revenue growth comparable to that of the other two sectors.

Unsurprisingly, real estate and steel were the worst performers. The former reported yoy declines of 23% and 97% in revenue and profit, respectively—while the latter saw corresponding drops of 9% and 93%. These two sectors, along with building materials, drove 110% of listcos’ revenue decline for the period and 70% of their fall in profit. Power equipment, another industry struggling with excess capacity, contributed to 35% and 60% of listcos’ revenue and profit declines, respectively.

Fossil fuels, which used to propel China’s industrial profits, now has less weight. With 3% less revenue and 6% less profit, both yoy, petro and coal together contributed to only 26% and 17% of the declines in listcos’ revenue and profit, respectively—far less than real estate, steel, and power equipment. In other words, if China’s policymakers succeed in reinvigorating other industries, a global fall in oil prices next year may not hit industrial profits as hard as has historically been the case. (See: Q&A: China’s Economy vs US Tariffs.)

Capex & leverage

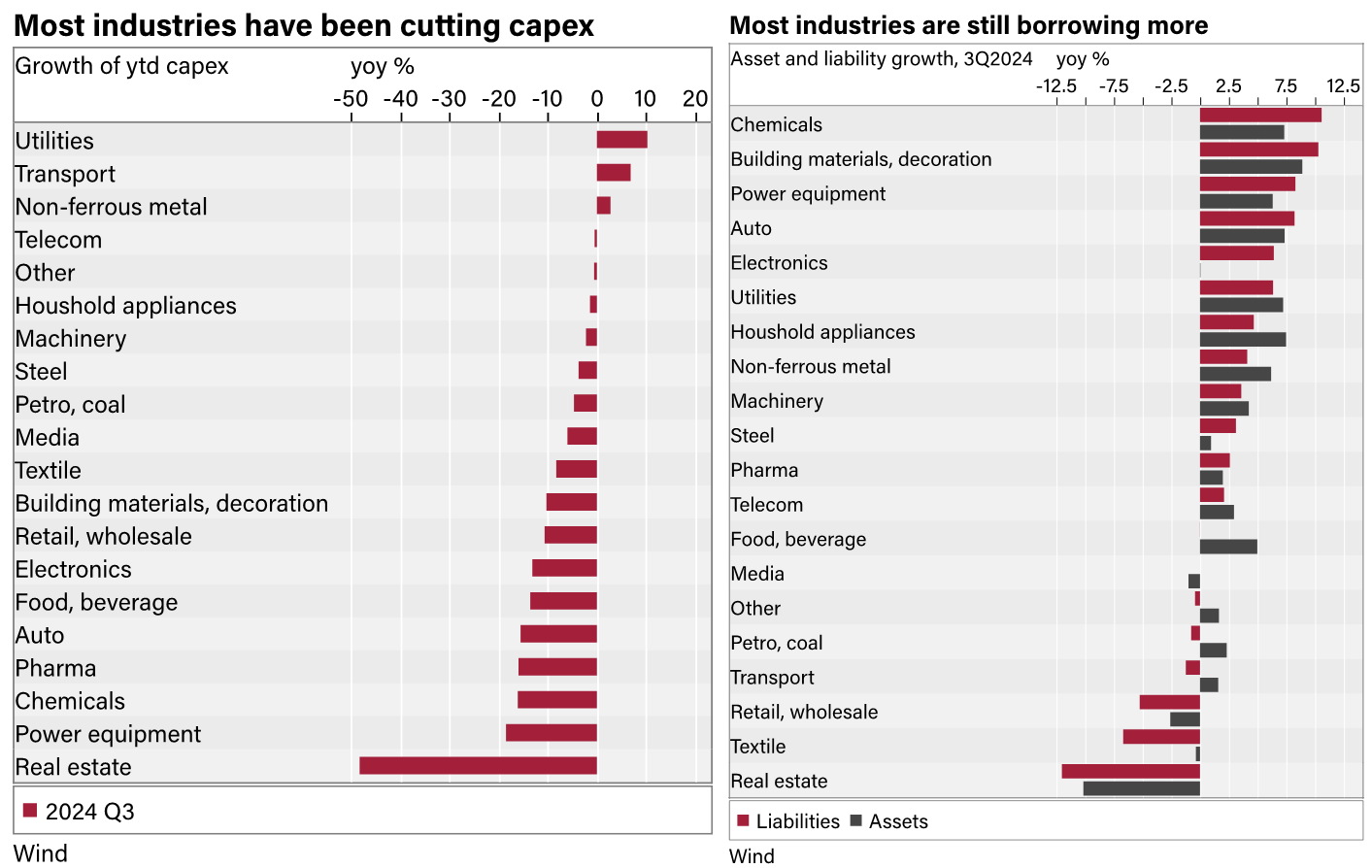

Amid such poor profits, it is also unsurprising that A-share nonfinancial listcos have been slowing capital expenditure (capex). In Q3, they recorded only RMB 1,028bn therein, down by 13% yoy and worse than Q2’s 10% yoy decline. This, too, differs from NBS data, which show 8.8% yoy growth in manufacturing investment for Q3. This disparity suggests that smaller firms, likely enabled by government support, are investing more aggressively than larger, more financially disciplined listcos.

Slower investment by listcos is evident in most industries. Real estate led the slowdown with year-to-date capex down by 48% yoy. Power equipment, chemicals, pharmaceuticals, and autos followed, each recording 15-20% yoy declines. Nonferrous metal rose only due to strong investment in gold, while utilities and transport grew by 10% and 7%, respectively thanks to government-led infrastructure investment.

This is not a balance-sheet recession, however. In fact, most industries are still borrowing more. Chemicals’ total liabilities increased by 11% yoy in Q3, and building materials’ by 10% yoy. Power equipment and autos also grew, both by 8% yoy, followed by electronics and utilities. Only real estate, textiles, and retail posted yoy declines over 5%. Total liabilities of all nonfinancial listcos increased by 2% yoy in Q3.

Listcos’ total assets also rose. Building materials led this with a 9% yoy increase, as firms booked more construction in progress. Household appliances, autos, chemicals, and utilities followed with 7% yoy growth each. All other industries minus real estate, retail, and media also recorded asset growth. As a result, the liability-to-asset ratio of A-share listcos—excluding real estate—increased by 0.2ppt yoy. With real estate included, it instead fell by 0.2ppt.

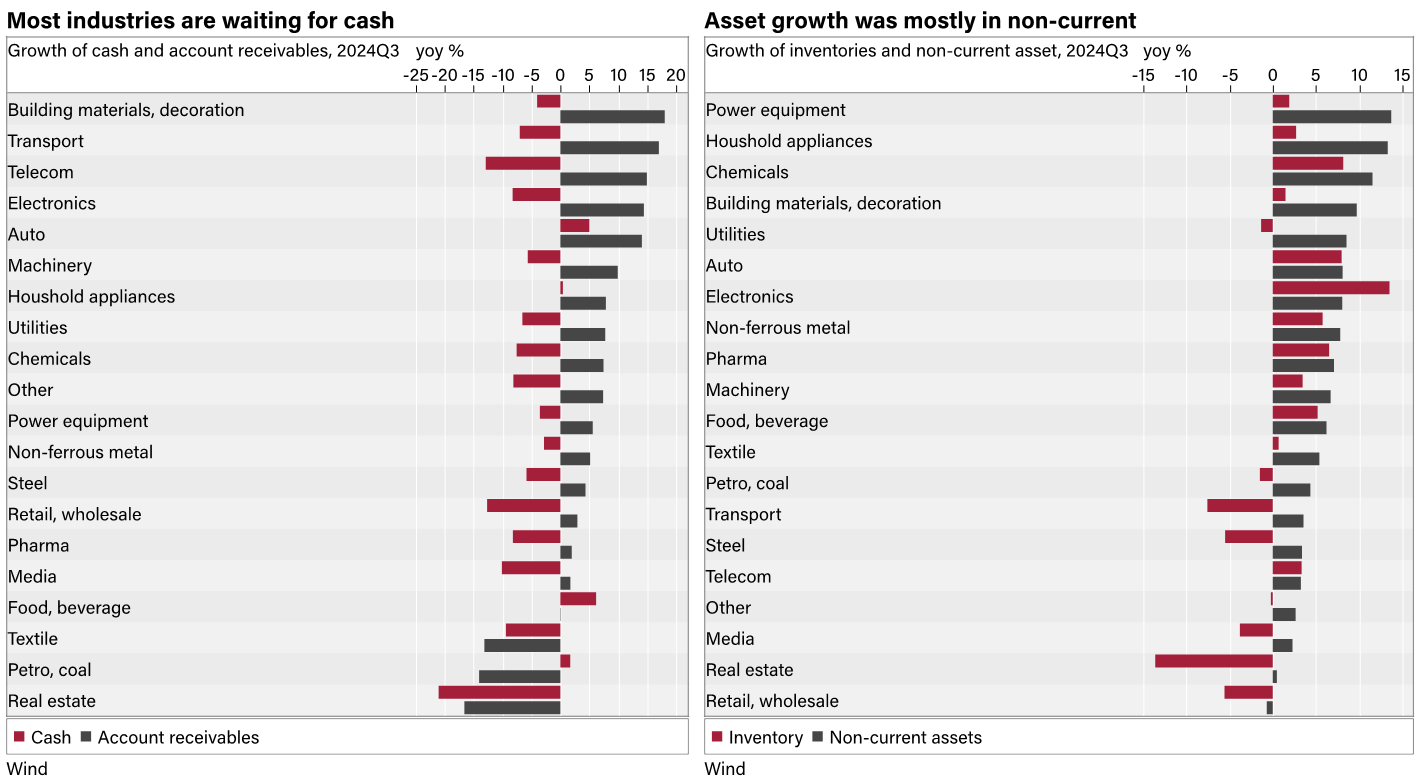

Nonetheless, low asset liquidity is still a problem. Of the 20 industries that we track, 14 recorded decreases in cash and increases in accounts receivable, both yoy, in Q3. 12 industries also saw their inventories climb. Altogether, nonfinancial listcos’ cash contracted by 6% yoy, while their accounts receivable swelled by 9% yoy. Excluding the 14% yoy ebb in real-estate inventory, other nonfinancial listcos’ inventories grew by a combined 2% yoy. Overall, more than 90% of listcos’ asset increases were driven by noncurrent ones, which naturally offer little to working capital.

Therefore, we believe just as firmly that Beijing’s focus on debt-mitigation will be more efficacious than direct fiscal stimulus. If larger and better-bargaining listcos find themselves short on cash, the situation for smaller firms will be even worse, especially given their zealous investment. With more cash freed up, economic confidence will rise, and then governments, firms, and households alike can all invest and consume with a greater sense of security.

IPOs & exits

For listcos, one of this year’s most noteworthy events was the appointment of Wu Qing as head of the China Securities Regulatory Commission (CSRC). Since taking the helm, he has launched various reforms aimed at strengthening supervision over A-share listed firms, with an explicit promise to delist problematic ones from the market.

52 firms have already exited China’s stock markets this year, already exceeding 2023’s tally of 45. Of these, 38 left after their stock prices fell below par value, versus last year’s 20. 14 companies failed to maintain required levels of profitability and / or information disclosure in 2024. Privatization and M&A, though common abroad, are rare as a means of delisting in China: The former has not occurred since 2013, while only 1-3 instances of the latter were seen annually over the past decade (with none this year).

Beijing appears to seek a larger role for M&A. Along with the People’s Bank of China’s (PBOC) announcement of stimulus on 24 September, CSRC set forth several measures to enhance listco value, with a focus on supporting M&A. (See: China Fires Stimulus Cannon.) On 1 November, regulators loosened requirements for foreign investors to make strategic investments in A-share listcos, even permitting overseas private company shares as payment. Further, on 15 November, CSRC issued a directive exhorting listcos to raise their valuation by means such as share repurchases, which has become more attractive in light of PBOC’s launch of relending facilities on 18 October.

Conversely, listing A-shares has become more difficult. Only 86 companies have got listed this year, after the CSRC tightened IPO and fundraising requirements in August 2023, versus over 300 per year over the prior three years. These 86 collectively raised only RMB 56bn, or an average of RMB 650mn per company. Thes figures are down significantly from last year’s RMB 360bn total and RMB 1.1bn per-firm average.

Some tightening is admittedly necessary. 300 annual listings comports with neither historical patterns nor a world currently seeing US policy rates above 4%. Indeed, China was the world’s largest IPO markets in 2023, with double the amount of capital raised in the US (the runner-up). This was particularly unjustified in light of A-share equities’ poor performance for the year.

Beijing’s anticorruption campaign in the financial sector also uncovered rampant rent-seeking in these IPOs. Since this October, four former officials from CSRC’s public-offering wing—and all closely tied to the Growth Enterprise Market, a submarket for small and medium-sized tech firms that do not qualify for the main board—have been detained for investigation. The Party’s anticorruption watchdog also removed Yao Qian, the former head of CSRC’s science and technology regulation department, for alleged abuse of power and accepting cryptocurrency as bribes.

Against this backdrop, two variables will likely determine the pace of China’s IPO market going forward: First, stock prices in the secondary market must be stabilized to allay Beijing’s concerns about investor sentiment—especially complaints that IPOs have been draining capital away from their existing holdings. Second, corrupt officials will need to be brought to light and disciplined to a level that meets Beijing’s comfort. This October, China concluded its formal anticorruption campaign in the financial sector—but it may yet take a few months for authorities to close cases and sort out the aftermath.

In case you missed our recent publications:

© Hutong Research. Redistribution prohibited without prior consent. This report has been prepared for distribution to Hutong Research clients. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. For more information and research archive, visit: www.hutongresearch.com