China Economy

Work For the Best, Prepare for All Possibilities

- China’s top leaders reaffirmed commitment to expanding domestic demand in 2025 on the annual economic conference

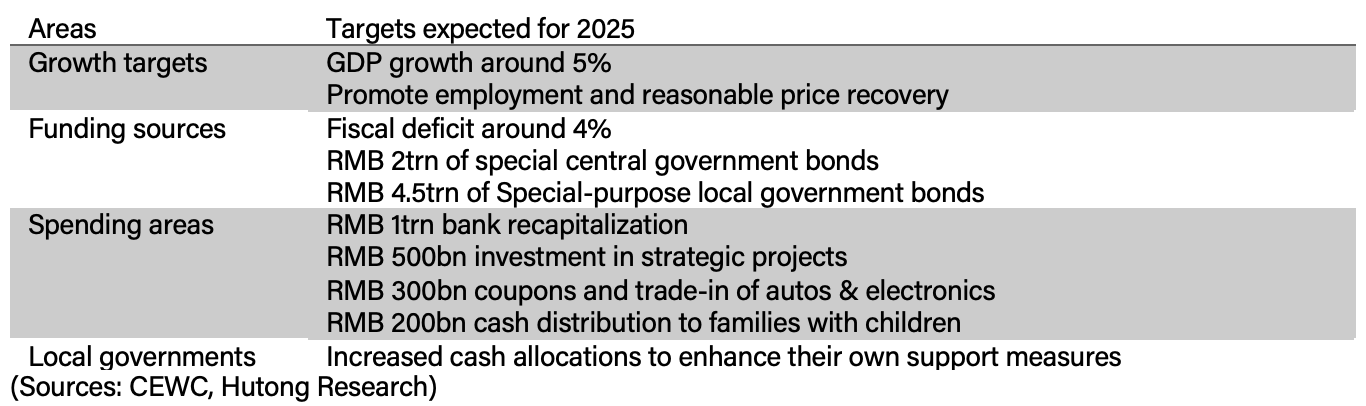

- We anticipate a growth target of around 5%, a fiscal deficit of approximately 4%, and increased issuance of central and local government bonds, to be announced in March

- A roughly equal focus on investment and consumption is expected, with consumption measures including service coupons and cash distributions to families with children

- We foresee faster deployment of local government bond proceeds, alongside stricter oversight of anti-competitive practices

- Beijing signaled greater tolerance for RMB depreciation against USD while maintaining stability of the RMB against a basket of currencies

- PBOC is likely to cut rates by at least 50bps in 2025, supported by more accommodative policy signals from the top leaders and the US Federal Reserve’s shift toward rate cuts

The Party held its annual Central Economic Work Conference (CEWC) from 11 to 12 December to outline economic policies for 2025 with a readout released on the night of 12 December. The readout highlighted the successes of stimulus measures announced since this September and reaffirmed commitment to delivering the targets set in the 14th Five-Year Plan. For 2025, the policy goals include promoting economic growth, ensuring employment, stabilizing prices, balancing international payments, and aligning household income growth with the country’s economic expansion.

The stimulus

The CEWC readout largely echoed key messages from this week’s Politburo meeting, which approved the Party’s policies priorities for 2025 (see: Beijing Raises Expectations to Drive Consumption). Comparing to the Politburo readout, the one from yesterday provided additional details on Beijing’s stimulus plan for next year, which we now anticipate will include increased central government bond issuance and direct cash distributions to households with children.

The readout explicitly committed to a “higher fiscal deficit,” “more issuance of ultra-long special central government bonds,” and “more issuance of special-purpose local government bonds.” Consequently, we expect Beijing to set a fiscal deficit target of approximately 4% in its government work report to be released next March, higher than 3.8% in 2023. We also forecast RMB 2trn in special central government bond issuance (up from RMB 1trn in 2024) and RMB 4.5trn in special-purpose local government bonds (up from RMB 3.9trn).

We particularly expect cash distributions to households, a projection that may diverge from broader market consensus. The readout emphasized boosting household consumption as a key driver of expanded domestic demand. While supporting low-income groups remains a focus, it also mentioned policies to “promote fertility.” A State Council notice from October had already pledged to develop maternity subsidies for families with children under three years old.

The readout also prioritized support for new infrastructure and urbanization initiatives (“two news”) and emphasized stimulation of consumption, especially service-oriented consumption. This likely entails expanded use of consumption coupons, such as restaurant coupons already being offered in Shanghai and Guangzhou for diners. Similarly, many cities are rolling out subsidies for electronics trade-ins, and last month, the Ministry of Commerce signaled the continuation of trade-in campaigns for automobiles.

At the same time, the CEWC underscored the importance of investment. It emphasized funding key projects and key sectors (“two keys”), noting the necessity of government investment to drive private sector participation. Key areas of focus include upgrading urban infrastructure, reducing logistics costs, and investing in green and high-tech industries, including the application of technologies such as AI.

Local governments are expected to supplement these efforts. With the debt-mitigation plan now in effect, provinces have significantly more cash available for spending (see: Q&A: China’s Economy vs US Tariffs). Over the past month, provinces issued RMB 2trn in bonds to address implicit debts and unlock funds for other priorities. Jiangsu led in bond issuance, followed by Hunan, Shandong, and Henan. Shanghai, Guangzhou, and Shenzhen have already cleared their implicit debts, so did not issue any such bonds.

Notably, 12 provinces, including Zhejiang and Shandong, have reportedly been granted the authority to determine how to allocate their special-purpose bond proceeds. This authority, previously contingent on approvals from National Development and Reform Commission and Ministry of Finance, often delayed fund deployment and led to mismatches between funding and projects. Delegating this power should expedite spending and investments.

That said, CEWC readout emphasized the need to rectify “involutionary competition” and ensure discipline in the behavior of local governments and enterprises. This suggests tighter oversight of government spending, likely through post-expenditure audits now incorporated into Beijing’s anti-corruption campaign, rather than pre-spending approval processes. Recent criticism of companies like PDD and BYD for pressuring vendors may become a focal point for enforcement actions.

PDD is in particular trouble for its “refund with no return” policy, which allows customers to receive a full refund for a product without needing to return the item, essentially allowing them to keep the product while getting their money back. This practice has been criticized by merchants as it puts a strain on their profits and is currently under scrutiny by Chinese regulators.

The risk

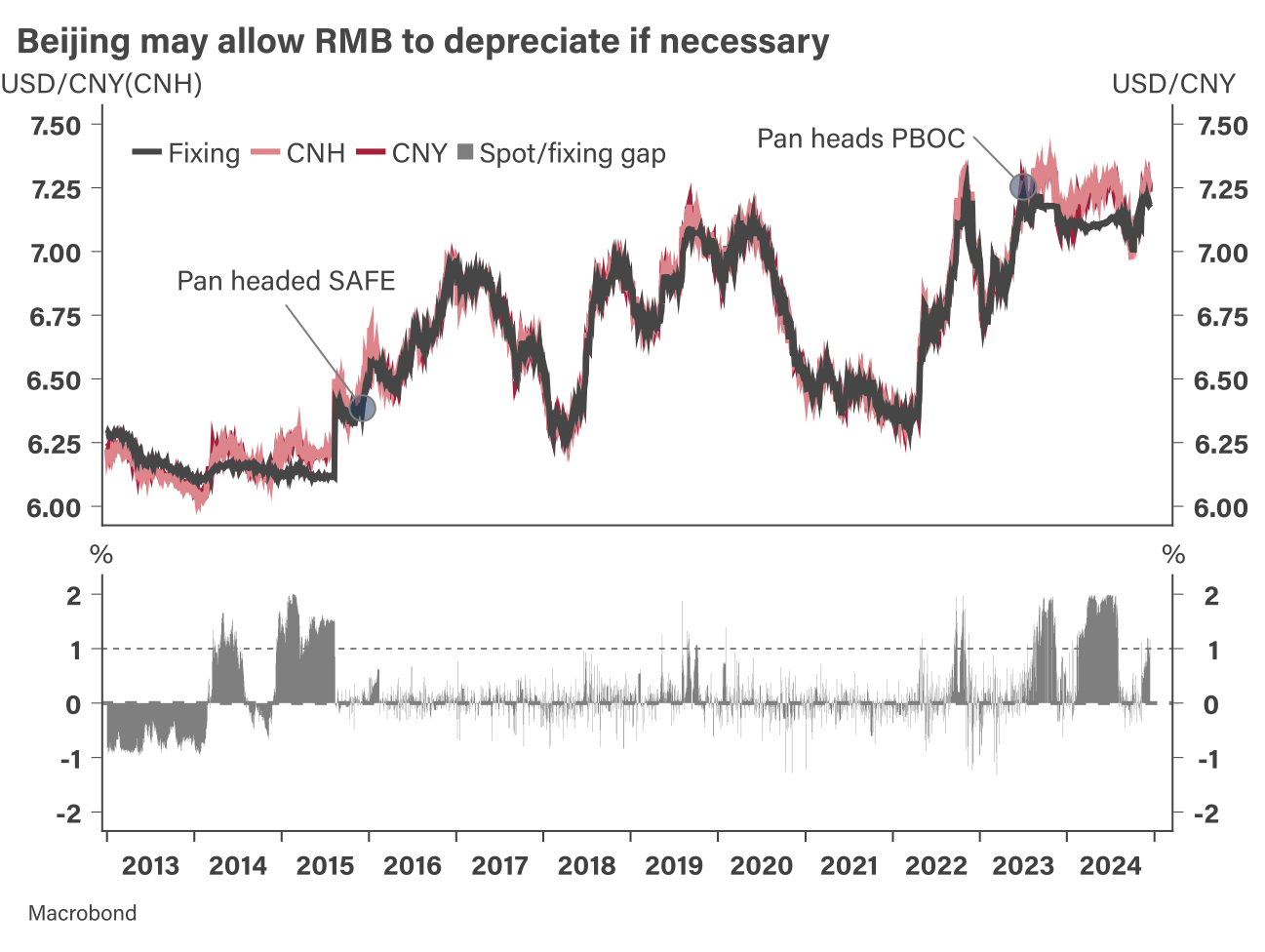

A surprising element of the readout is its emphasis on balancing China’s international payments. While this may seem like a reasonable objective, the term had rarely appeared in CEWC readouts, surfacing only once in 2014. The subsequent year saw significant turbulence, including a stock market crash and the sudden liberalization of the exchange rate in August 2015, which triggered a 15% depreciation of the RMB between then and December 2016. This period also ushered in tighter capital controls. If similar conditions arise, USD/CNY could rise from 7 to 8, prompting Beijing to reintroduce capital controls.

Pan Gongsheng, the governor of People’s Bank of China (PBOC), played a pivotal role in managing RMB depreciation in 2016 after his appointment as State Administration of Foreign Exchange (SAFE) administrator in January that year. However, the liberalization of RMB in August 2015 occurred under then-SAFE administrator Yi Gang. Both Pan and Yi were later promoted to the role of PBOC governor, reflecting Beijing’s acknowledgment of their efforts in navigating monetary policy and exchange rate challenges.

The renewed focus on balancing international payments suggests Beijing may now be more tolerant of RMB depreciation. Since October, the PBOC has raised the USD/CNY fixing rate, resulting in a spot rate that is only 1% above the fixing—well below the 2% ceiling. By comparison, the PBOC maintained USD/CNY at around 7.1 until August this year, even as spot rates fluctuated near the ceiling.

That said, a PBOC’s news outlet article from two days ago emphasized that there remains a solid foundation for keeping the RMB exchange rate “basically stable.” The article attributed recent depreciation to speculation around a stronger USD and warned of potential reversals as China’s economy recovers.

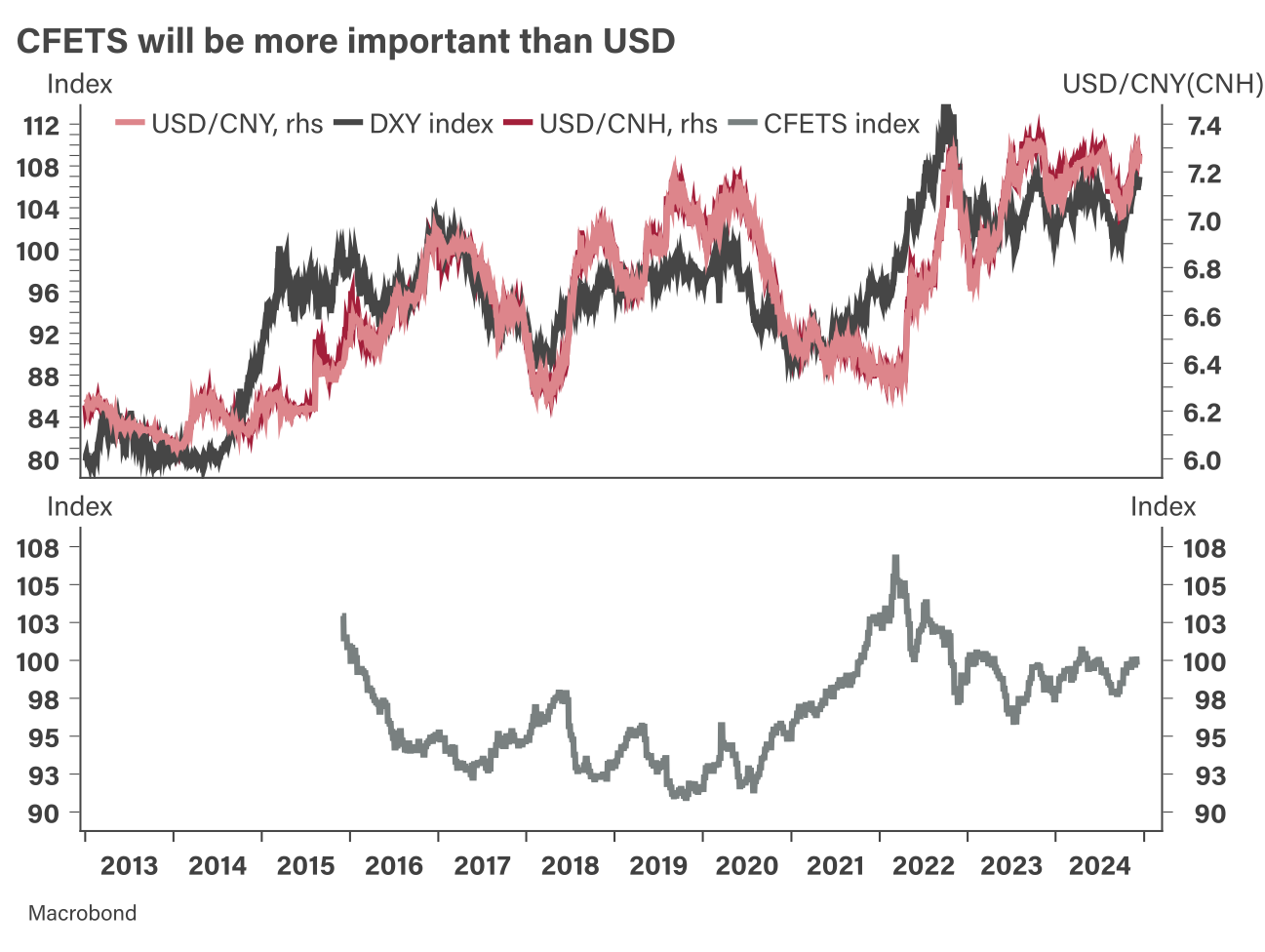

This argument holds merit. The RMB’s depreciation has been closely correlated with USD appreciation, as reflected in the DXY index, which measures the dollar’s strength against a basket of currencies. Meanwhile, the RMB has appreciated against the currency basket, as indicated by the CFETS index. Over the past year, the CFETS index has fluctuated within a narrow range of 98 to 100, signaling relative stability compared to other currencies.

This contrasts sharply with 2016, when CFETS index dropped from 103 to 95 within a year. At that time, RMB depreciation significantly impacted China’s trading partners by making Chinese exports cheaper than theirs. Today, Beijing appears committed to maintaining CFETS stability, even if USD/CNY fluctuates, to improve trade and investment relations with other countries. This intent was underscored by Beijing’s recent decision to reduce export-tax rebates for products subject to overcapacity complaints.

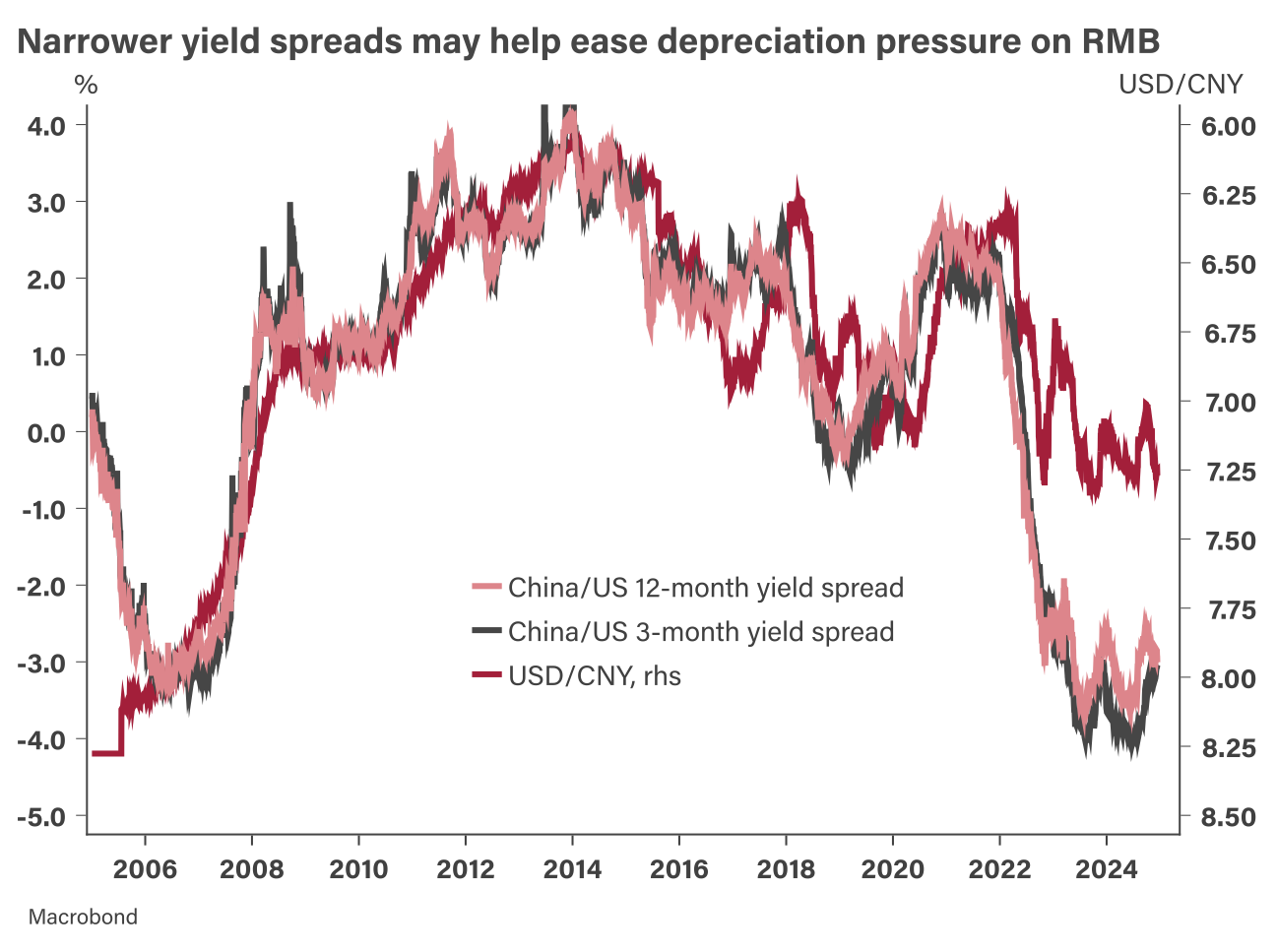

Additionally, the Federal Reserve’s recent rate cuts could alleviate depreciation pressure on the RMB. Although China’s bond yields have fallen recently, the yield spreads with US bonds remain relatively stable and narrower than six months ago. As the US implements more rate cuts, RMB depreciation pressure may ease further.

Finally, if Beijing succeeds in expanding domestic demand, the RMB could remain resilient even as the PBOC lowers rates, especially with the fiscal impulse. Currently, policy rates are too high relative to deflationary producer prices and declining corporate profits. This mismatch discourages borrowing and investment, ultimately constraining economic recovery, foreign capital attraction, and RMB stability.

China’s leadership appears increasingly receptive to this argument. The recent Politburo meeting pledged to “stabilize housing and stock markets” and “improve returns on investment.” Meanwhile, the CEWC committed to further cuts in policy interest rates and reserve requirement ratios, alongside efforts to promote a reasonable recovery in prices. Given these developments, we expect the PBOC to implement at least 50bps of cuts in 2025, compared to 35bps so far this year.

In case you missed our recent publications:

© Hutong Research. Redistribution prohibited without prior consent. This report has been prepared for distribution to Hutong Research clients. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. For more information and research archive, visit: www.hutongresearch.com